When it comes to property investment, the first thing that you must very clear of is neither what to buy nor where to buy, but your EXIT PLAN. You must know what is the objective of your investment. Could it be flipping or rental collection?

What is flipping? Flipping is basically buy and sell for a quick profit after the property appreciates for a certain percentage or an amount sum of RM150,000 for instance. There is no right or wrong in the amount that one is targeting. Some people would want a 20% appreciation but another individual would want a 50% profit. On the other hand, some investors would prefer to keep the property for long term rental collection. Therefore, which strategy suits your personality better?

Today, we would like to share some of our opinions with you when it comes to deciding whether the property is suitable for flipping or for rental. For example, a landed property in most of the places in Malaysia does not give a very promising rental income. The rental could only cover probably 50% or less of your monthly repayment to bank. However, if you look at the property value appreciation, it could give you a very good profit of 30-50% in a very short period of time depending on its location. Now let's look at the rental option. If you have a property in Bukit Bintang, KLCC, Bangsar South, Mont Kiara or KL Sentral where you have a lot of expatriate tenants and job opportunities within the vicinity, then we can see that there could be a very good rental return yield of 5-8%, which is more than enough to cover your bank interest of 4.4% +/-. For this type of property, you may consider keeping it for a very long time because the rental could at least cover your monthly repayment or even get you a positive cash flow after deducting other expenses if you know how to pick the right property.

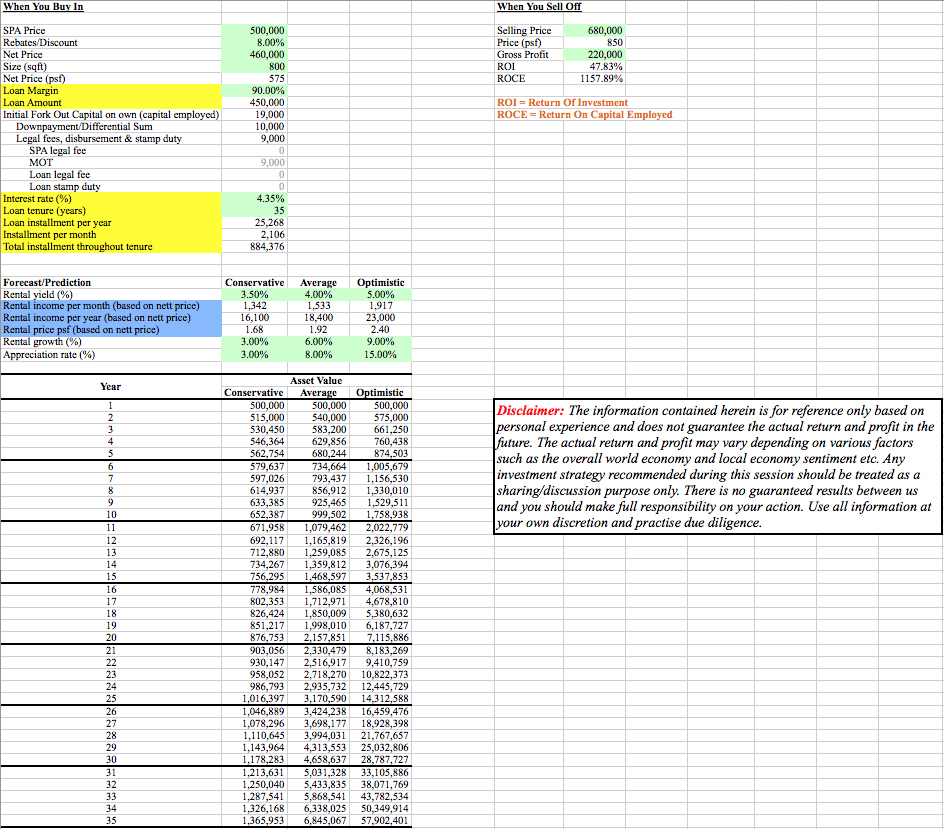

For a quick discussion, we take an example of a RM500,000 property for our case study. Mr X approached us to find him his first house. With our assistance, we are able to get him an early bird deal. Given 8% rebates and FREE SPA & loan legal fees as well as Loan Stamp Duty. He only needs to fork out RM19,000 to own this property. Stretching to a maximum loan tenure of 35 years, he is paying an instalment of RM2,106 per month.

As per shown above, we made an assumption and forecast on 3 different scenarios, Conservative, Average and Optimistic. With our country economic growth and property market outlook, a 3% appreciation rate is quite unlikely, given the inflation rate is already about 3~6% annually. Thus, if you have a salary increment of 3-5% annually, you better think twice and discuss with you higher management! You might not be getting an increment actually. When the market was booming around the year 2010-2013, we noticed that the appreciation rate in Klang Valley could be as high as 15~20% annually. However, those days were gone for now, but will it be back in a few years time perhaps? So, an average of 7~12% appreciation should be a comfortable range for our discussion today.

Looking at the Average scenario, let us assume an average appreciation of 8% each year, the value has appreciated to around RM630k and RM680k somewhere between the 4th and 5th year. Let's say Mr X sells his property for RM680,000. He would be making a gross profit of RM220,000 (because he is entitled for the early bird rebates, his net purchase price was RM460,000). The gross ROI for his investment is 48%, and his gross ROCE is a whopping 1158% because he only forks out RM19,000 capital upfront to buy this property.

Would you want to make the same kind of investment return?

Let's talk about the rental part now. As an investor, you have to research on the current rental market rate going on within the same vicinity of the property that you are going to purchase. Despite just by pure looking at the rental rate, you have to analyse the age of the building, facilities provided, tenant crowd, property management team etc. This is because as far as lifestyle and safety is concern, different condominium would definitely give you different rental rate. After having done that, you have to justify against your data again.

For instance, if the average rental range for the same "standard of living and lifestyle" with the property that you are considering is currently going at RM1.50-2.00 per sqft (depending on furnishings and view etc). With a reference to our assumption of Average scenario, 4% rental yield would give you a RM1.92/sqft. Bare in mind that we are talking about the rental rate 3 to 4 years later. So would you think a minimum 4% rental yield is confidently achievable? What about 5% rental yield? You judge yourself.

Have you ever thought on how could you make your unit stands out from the others and rent it out at a higher rate (more than 5%)? We have seen quite a number of cases. Check it out from us if you would like to know more.

~~~ "PROPERTY INVESTMENT IS THE BEST HEDGE AGAINST INFLATION" ~~~